In March, the U.S. Securities and Exchange Commission (SEC) finalized rules requiring companies to disclose to regulators their greenhouse gas (GHG) emissions and transition plans for lowering them. The new rules, set to go into effect in 2026, are currently in legal limbo amid numerous challenges, including whether the SEC even has the authority to set such requirements. However, other countries as well as some US states are charging ahead on a slew new mandatory climate mandates that will impact US companies up and down the supply chain, including agriculture, regardless of the fate of currently contested regulations at the Federal level.

According to recent research from the World Resources Institute, rules that are already in force or pending are set to be enforced on around 40% of the global economy. The EU’s regulations are expected to be some of the most stringent so companies that depend on the bloc’s business are going to be the hardest hit. WRI estimates some 10,000 non-EU headquartered companies will be affected, with an estimated 3,000 located in the US.

Here at home, California’s proposed climate disclosure rules are expected to impact around 10,000 US-based companies. Other states are following California’s lead, too, including New York and Illinois, with more expected to jump on the bandwagon.

One of the most contentious issues among this cornucopia of climate mandates is so-called “Scope 3 emissions.” For those not familiar, “Scope 1” covers emissions from sources that an organization owns or controls directly – for example from burning fossil fuel in fleets of vehicles. “Scope 2” are indirect emissions resulting from its energy use. “Scope 3” 3 encompasses emissions that are not produced by the company itself and are not the result of activities from assets owned or controlled by them, but by those that it’s indirectly responsible for up and down its value chain. Essentially, it’s an umbrella for anything and everything not included under Scope 1 or 2.

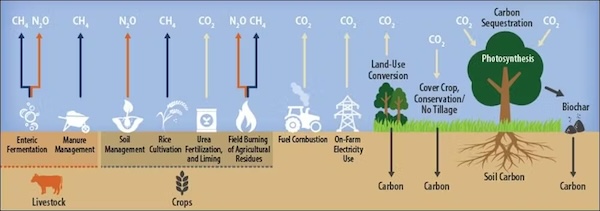

Scope 3 emissions on the farm occur both upstream and downstream. Upstream emissions include all bought-in inputs such as manufactured fertilizer, imported feed and machinery and equipment, and transport of supplies. Downstream emissions include packaging, packing and distribution, and food preparation and cooking.

Things start to get ridiculously complicated and burdensome the further you go up the supply chain. For instance, Scope 3 emissions for food companies include all of the emissions generated by producers. Ultimately, this means the Scope 3 category represents about 90% of overall emissions in the food industry. This also means that food companies will likely be under pressure to source their commodities from farmers that are using so-called “climate friendly” farming practices.

While the SEC’s pending rules no longer include Scope 3 emissions reporting, experts say that most of the new and pending regulations from other authorities do. As of right now, California, the EU, the UK, China, and Australia have all opted to include Scope 3 emissions data in their proposed regulatory frameworks.

Interestingly, many legal experts believe that these rules may not be strictly enforced, especially in the EU with regard to non-compliant companies that are headquartered outside the bloc. However, experts also warn that companies choosing not to comply run the risk of losing business to those that are prepared to jump through the regulatory hoops. (Sources: Thomson Reuters, Inside Climate News, SustainableViews)