The National Cattlemen’s Beef Association (NCBA) spent nearly a year collecting responses from members regarding the importance of key provisions of the 2017 Tax Cuts and Jobs Act (TCJA), which is set to expire at the end of 2025. Around 99% of respondents identify their operation as family-owned, regardless of legal structure, and 64% are third-generation cattle producers or greater.

“When I was starting out in the ranching business, I saw the devastating impact of the Death Tax firsthand and this tax nearly killed my dream of ranching with my family,” said NCBA President and Wyoming rancher Mark Eisele. “This experience pushed me to fight for lower taxes on farms and ranches, and the data collected by NCBA shows that many other producers around the country have faced similar pressure from devastating tax bills too. I urge our policymakers to see the story this data is telling—that farmers and ranchers need lower taxes to stay in business and continue feeding the world.”

The “Death Tax” that Eisele refers to are taxes imposed by the federal and some state governments on someone’s estate upon their death. These taxes are levied on the beneficiary who receives the property in the deceased’s will or the estate that pays the tax before transferring the inherited property.

Most people end up not paying estate tax because it applies to only a few people. This is because the 2017 Tax Cuts and Jobs Act (TCJA) applied the estate tax to the basic exclusion amount, which in 2023 is $12.92 million and in 2024 is $13.61 million. However, this number may drop after 2025 if Congress doesn’t renew the TCJA. Most expect the estate tax threshold will then revert back to pre-TCJA levels of $5.5 million for individuals and $11 million for couples.

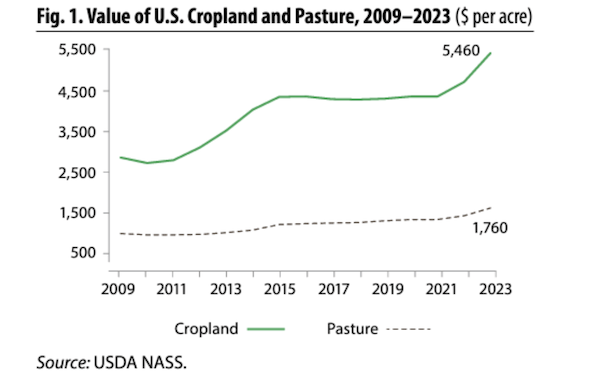

But ranchers and farmers are not most people. According to NCBA, the value of real estate is often a producer’s greatest asset. The sale of farmland can generate a hefty capital

gains tax which can cripple operations that have limited cash flow.

Of those responding to NCBA’s survey, over one-third of respondents have been impacted by the estate tax; and of those respondents, 35% have been impacted more than once. In addition to the federal estate tax, 40% of respondents anticipate being subject to state-level estate tax. This helps explain why 27% of respondents believe the estate tax is their greatest tax concern. In contrast, USDA reports that between 1934 and 2016 only 1.8% of adults generated a taxable estate valued above the exclusion amount, and that number has fallen to 0.1% in recent years.

NCBA survey results show that some respondents have allocated significant financial resources to comply with the estate tax and protect their business. For example, 18% of respondents have been forced to sell land, livestock, or other assets to pay for the estate tax, and 9% have taken out a personal loan or lien to pay for the estate tax. Sadly, 25% of respondents were prevented from investing in their operation due to the estate tax.

If the current estate tax limits established under the TCJA are allowed to expire, 61% of NCBA survey respondents will be impacted. NCBA notes that this figure contrasts with USDA’s broad estimate that only 1% of farm estates will be subject to the estate tax if the threshold is reduced to previous levels.

The survey data also revealed widespread support for key tax provisions that reduce financial burdens on producers. These include the 1031 Like-Kind Exchange, Section 179 Expensing, Bonus Depreciation, and Section 199A Small Business Deduction. The report underscored that a quarter of respondents spend over $10,000 annually on tax preparation, filing, and potential audits—costs that place additional strain on agricultural operations.

Kent Bacus, NCBA’s Executive Director of Government Affairs, emphasized the importance of maintaining these tax provisions to support the unique challenges faced by cattle producers. “Farms and ranches are not like other businesses,” Bacus noted. “Congress must protect tax policies that enable producers to reinvest in their operations and set up future generations for success.” Learn more at NCBA.