California has led the nation in building demand for renewable diesel, with nearly all US production consumed in the state. The legislation largely responsible for this is California’s “Low Carbon Fuel Standard” (LCFS), which incentivizes demand by providing carbon credits for low-carbon and renewable alternatives. Now, state officials are considering capping the amount of renewable diesel made from soybean and canola oil that would qualify for the LCFS credits, a move that could have widespread implications for the renewable diesel industry, as well as U.S. farmers.

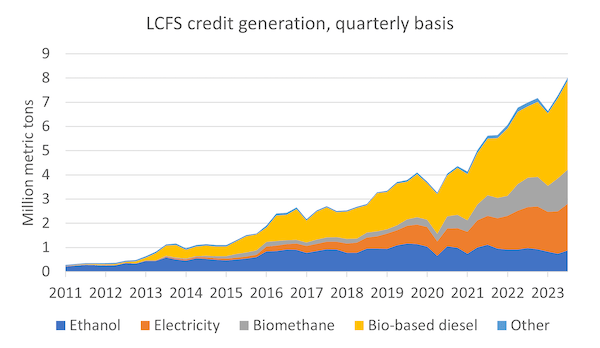

Under new proposed rules from the California Air Resources Board (CARB), companies would be eligible for LCFS credits on no more than 20% of biomass-based diesel that comes from soybean or canola oil. According to Scott Gerlt, an economist for the American Soybean Association, biofuel sourced from soybean and canola oil accounted for about 30% of the renewable diesel that qualified for LCFS credits during Q1 2024.

The proposal also would likely increase credit prices and boost fuel costs in the state, according to Gerlt. Additionally, the cap “will lower the amount of credits that can be generated, which will pull back the supply somewhat and increase the credit price,” explains Gerlt.

California’s LCFS standards are expressed in terms of the “carbon intensity” (CI) of gasoline and diesel fuel and their respective substitutes. The carbon intensity scores assessed for each fuel are compared to a declining CI benchmark for each year.

The 2019 benchmark was a -6.5% reduction from 2010, and the 2030 target is a -20% reduction. In January 2024, CARB proposed to increase the 2030 target to -30%, with a one-time -5% reduction in 2025. The proposed changes would also extend the declining CI targets through 2045, which would be a -90% reduction by then.

The LCFS currently requires fuel makers to buy tradable credits if their products generate more carbon emissions than the baseline set by regulators. Refiners that produce low-carbon fuels and gases can generate credits to sell. LCFS credits don’t expire and can be banked for future use.

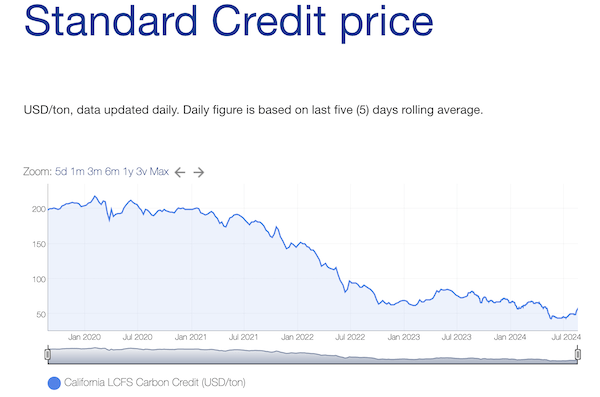

However, prices for the state’s carbon credits have plunged from as high as $200/ton in 2018 to around $50/ton in mid-August 2024. This is blamed on a steep increase of biomass-based diesel that critics say has left the carbon credit market oversupplied. Plunging credit prices in turn reduce the incentive for producers and end-users alike to seek out even lower carbon alternatives, according to critics.

However, CARB’s thinking on various feedstocks seems wrong-footed. For one, much of the pushback on “virgin biomass”-based biofuels, particularly soybeans and canola, is based on the assumption that they require clearing of new land. While this may be true in some South American and Asian countries, it hardly applies to US production, where if anything, producers use less land than ever to grow crops. While CARB’s latest proposal for LCFS credits would allow producers to certify the origin of their feedstocks and likely provide US production better CI scores, soybean and canola feedstock use would still be capped at 20%.

Because California, Oregon, and Washington are the only states with active clean fuel programs that incentivize the consumption of renewable diesel beyond the incentives provided by federal policies, renewable diesel is primarily consumed on the West Coast. But a large share of that fuel is imported.

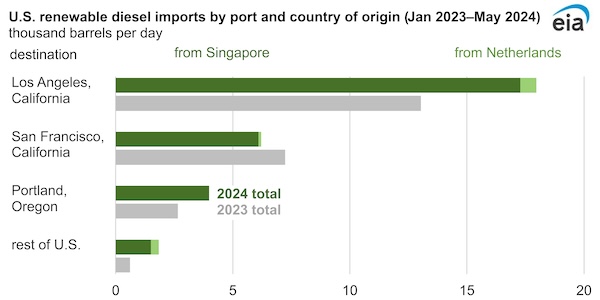

In the first five months of 2024, U.S. imports of renewable diesel averaged 30,000 barrels per day (b/d), up nearly +30% from 2023 May 2023. Most of the imports (94%) were destined for the U.S. West Coast. Those imports all came from Neste’s plants in Singapore and Rotterdam, according to the US Energy Information Administration (EIA). Additionally, EIA data shows imports accounted for 20% of U.S. consumption of biomass-based diesel from January through May. That’s up from a market share of 15% for the same period in 2023 and 10% in 2022.

US agricultural stakeholders also point out that the caps on virgin biomass incentivize California producers to turn to used cooking oil (UCO), which qualifies for larger financial incentives under LCFS. The ag industry already knows this is hugely problematic due to speculation that much of the UCO being brought into the country is fraudulent. Most likely, it is virgin palm oil that is associated with massive deforestation and pollution in many parts of the world. The US Environmental Protection Agency is currently investigating UCO sourced from Asia and there is talk that some sort of import ban may be put in place.

In addition to limiting virgin biomass use in renewable fuels, CARB is also proposing to phaseout LCFS crediting for renewable natural gas (“RNG”) projects after 2040, impose new limits on RNG injected into the common carrier pipeline network that could severely restrict the eligibility of out-of-state projects to generate LCFS credits, and eventually phaseout avoided methane crediting for RNG projects. The latter applies dairy, beef or hog producers that capture methane, mainly via methane digesters.

To be fair, California designed the LCFS program to gradually phase out combustion fuels in transportation and has been upfront about its goal of 100% electric vehicle (EV) sales for passenger vehicles by 2035 and 100% zero-emission heavy-duty truck sales by 2036. Critics argue that the LCFS program’s current support of biofuels is incompatible with the primary goal of boosting electric vehicle use. (Sources: Reuters, Farmdoc, Vinson & Elkins, CARB)