The US beef cow herd started the year with the smallest numbers since 1962 thanks to severe drought conditions that have plagued at least 40% of the country since September 2020. Drought conditions have dramatically improved but the US beef herd is still expected to shrink even further due to a combination of ongoing drought in key regions and lingering impacts where conditions have improved. At the same time, herd culling is expected to decline as producers begin to rebuild the herd, potentially setting the US up for a beef supply shock and a return of sky-high prices at the grocery store.

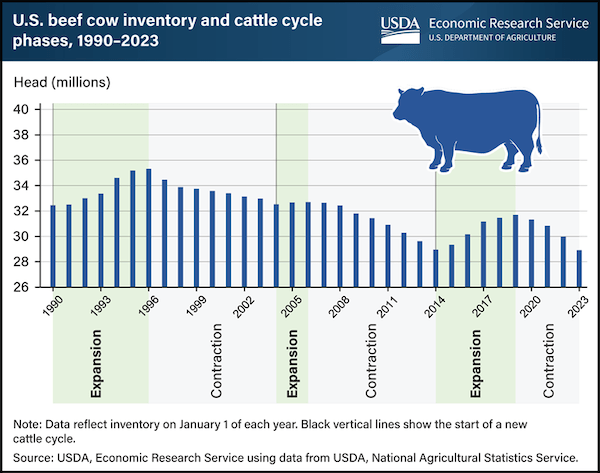

It probably comes as no surprise to cattle producers that herd culling hit record levels in 2022, which included some 13.4% of the US cow herd being liquidated. The estimated number of beef cows as of January 1, 2023, was 28.9 million head, down -3% from the previous year. The US Department of Agriculture (USDA) in February noted that producers expressed their intentions to retain the fewest heifers since 2011, which was during the last drought-fueled contractionary period of the last cattle cycle in 2004-2014.

For those not familiar, the cattle cycle is a process in which the size of the national cattle herd—including all cattle and calves—increases and decreases over time. The cycle averages 8–12 years, from low point to low point. Last year marked the 9th year of the current cycle and the 4th year of cattle inventory contraction.

During the last cattle cycle, inventory lows weren’t hit until 2014, a direct result of the cow slaughter acceleration that occurred in 2011, which in turn reduced the following years’ calf crops. The calf crop in 2022 of 34.46 million was comparable to 2012 output. But in the last cycle, the calf crop continued to shrink for another two years, hitting a low of 33.52 million in 2014 even as heifer slaughter continued to decline.

USDA says the fast pace of cow liquidation last year indicates that US producers are not optimistic about growing their herds in 2023. Rabobank analysts actually believe it will be 2025 before “meaningful” rebuilding begins, with a lack of breeding females likely being the limiting factor.

For producers in the Southern Plains, herd rebuilding may not even be on the radar yet as severe drought continues to impact the region. At the same time, the impacts of the drought are likely to linger for those that have finally gotten some rain, including poor pasture conditions and low hay supplies.

In the latest “Livestock, Dairy, and Poultry Outlook,” the USDA said that unexpectedly high feedlot placement levels in March—combined with poor forage and small grains pastures—suggest an

increase in anticipated placements in second-quarter 2023. Beef production in 2023 is forecast at 26.92 million pounds, down almost -7% from 2022. Assuming a return to normal pasture conditions, fewer cows and bulls are expected to be in the slaughter mix in 2024 as producers hold back animals for herd expansion. As such, production is forecast to fall a further -8% in 2024, which USDA projects will push cattle prices to new highs.

The annual fed steer price is raised about $2 for a projection of $166.50 per cwt in 2023, which is +15% above last year. In 2024, packers will likely have to bid higher for the shrinking slaughter-ready cattle supply. Prices are projected to average $172.00 per cwt for the year. Based on recent price data and declines in forecast corn season average prices, 2023 prices for feeders is estimated at $205.40 per cwt, a +24% increase from last year. Demand for feeder calves will continue in 2024, with prices forecast to hit $221.00 per cwt, a +7% year-over-year increase. Meanwhile, cull cow prices in 2023 are forecast to be $99.20 per cwt, an increase of +26% from 2022. In 2024, a decline in cull cow slaughter is expected to lift prices to $113.00 per cwt, a year-over-year increase of +13%.

That contraction in beef production means higher imports in 2023 and 2024. In fact, USDA forecasts imports will exceed exports both years. The annual forecast for 2023 is 3.501 billion pounds, a year-over-year increase of about +3%. While higher imports and lower prices for feed will work to keep a lid on prices, consumers are still likely to be paying more for their favorite beef cuts for at least another year or two. However, the next couple of years should be profitable ones for US cattle producers. (Sources: USDA, Rabobank, Food and Environment Reporting Network, Drovers)