CORN bulls are pointing to a few uncertainties in the U.S. forecast and some companies using high-tech geospatial and remote sensing technology that are forecasting the early U.S. yield at between 172 and 175 bushels per acre vs. the USDA’s current 178.5 yield forecast. Bulls also point to the continued talk of more unplanted acres shifting to soybeans or “prevent planting”. Bottom-line, bulls are thinking the USDA’s May total production forecast will be the largest of the year and the balance sheet should start shrinking a bit from here forward. Unfortunately, with ending stocks forecast at +3.3 billion bushels it is going to take a sizeable weather worry to put the balance sheet in a forward-looking position to attract larger bullish fund interest. On the demand side of the equation, data is showing ethanol demand improving as the U.S. economy comes back online, but many inside the trade suspect the USDA still has another -50 to -100 million bushels to cut from their demand estimate.

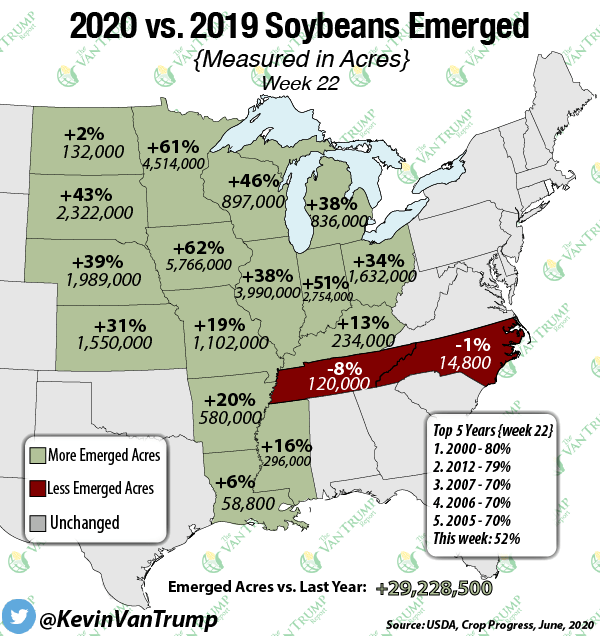

SOYBEAN traders are now caught trying to differentiate what’s real and what’s “fake news”. One minute the Chinese are suspending U.S. purchases, the next minute the USDA is announcing confirmed purchases by the Chinese. As a spec, I got spooked and exited my bullish position just ahead of yesterday’s nice rally because I was struggling to tell the difference between the rumors and facts. Many of the best inside the trade seem to have very little edge. Some of the most experienced and veteran traders I know are scratching their heads and uncertain about the next 30 to 60 days. At the same time, there’s talk that U.S. acres could move even higher. If U.S. weather cooperates, that means total production could move higher. Here we sit going into another summer trying to predict U.S. weather and U.S.-Chinese trade relations. Both are two headlines extremely difficult to bet on…

WHEAT bulls are pointing to hot and dry weather across the southern Plains. The trade is hearing that yields out of southwest Oklahoma are poor but I think most inside the trade have been anticipating. Bears are pointing to improved weather across many parts of Europe and the Black Sea region. Globally, the low-cost exporters remain Russia, Ukraine, and France, all of who Egypt sourced wheat from earlier this week.