As farmers are well aware, ag commodity prices have plunged from the peak levels reached in 2022. Unfortunately, new projections University of Missouri’s Food and Ag Policy Research Institute (FAPRI) indicate that the downward slide may continue though 2024 and possibly beyond.

FAPRI’s recently released baseline projections for agricultural and biofuel markets shows lower commodity prices and tight margins are expected for some U.S. farmers and ranchers this year. While market uncertainty persists, projected prices decline further for crops harvested in 2024, and net farm income falls to the lowest level since 2020.

“Despite a $30 billion drop in net farm income from 2022 to 2023, and another large projected decline in 2024, net farm income remains above annual levels from 2015 to 2020,” FAPRI director Pat Westhoff notes. “Still, there’s no question that farm finances are much tighter now than they were just two years ago.”

FAPRI points to the ongoing decline in crop prices that is placing pressure on profitability for farmers. “In 2023, we saw crops overcome challenging growing conditions and achieve significant production levels that caused a decline in prices. FAPRI research economist Bob Maltsbarger said. “Another year of trend-line yields, and shifting of planted acreage for key crops, could continue the downward trend of prices.” The full report is available HERE. Below are some of the highlights.

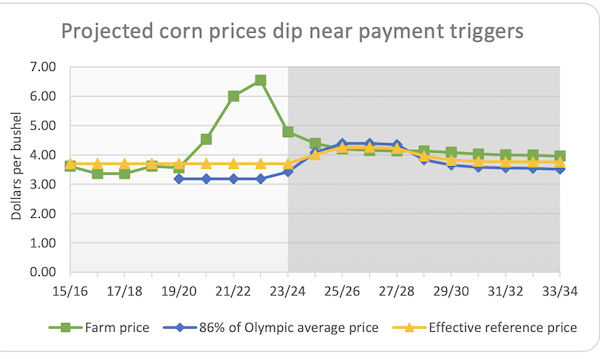

Prices for those major field crops have come back down from peak levels in 2021 and early 2022. For crops harvested in 2024, FAPRI says projected prices are near the average prices received by farmers between the 2014/15 and 2022/23 marketing years.

- U.S. corn production hit a record high in 2023, in spite of less than ideal growing conditions. Corn prices that averaged $6.54 per bushel in 2022/23 fall to a projected $4.39 per bushel in 2024/25 and even lower in later years.

- U.S. corn production hit a record high in 2023, in spite of less than ideal growing conditions. Corn prices that averaged $6.54 per bushel in 2022/23 fall to a projected $4.39 per bushel in 2024/25 and even lower in later years.

- Changes in relative prices cause an acreage shift from corn to soybeans in 2024, resulting in record U.S. soybean production.

- Rising production of renewable diesel increases demand for soybean oil and other fats and oils. This supports soybean oil and soybean prices, but the resulting increase in crush puts downward pressure on soybean meal prices.

Hog, chicken and milk prices all declined in 2023 and are expected to remain well below their peak values in 2024. The major exception to this pattern is cattle. Drought and other factors have reduced beef cow numbers, and beef production is projected to decline again in 2024. This has resulted in higher prices for both feeder and slaughter cattle.

- Hog, poultry, and milk prices all declined in 2023 as demand weakened. Projected hog prices are about the same in 2024 as in 2023, while further small declines are expected for poultry and milk prices. Lower corn and soybean meal prices mean lower feed costs.

- In contrast, cattle prices increased in 2023 and further increases are expected in 2024 and 2025. Drought and other factors have reduced the cow herd, and it will take time before beef production can increase again.

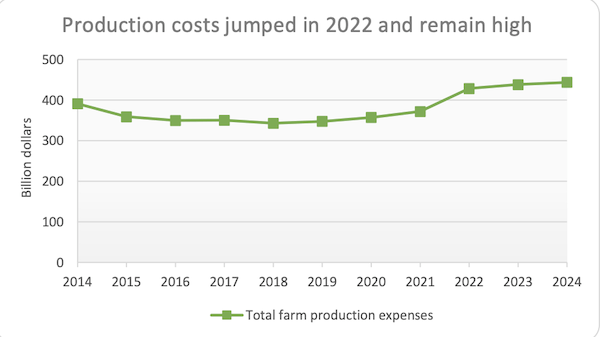

On the input side, FAPRI says the increase in production costs has slowed since 2022. However, higher interest rates, labor costs, and prices for purchased livestock have more than offset the impact of lower fertilizer and feed prices. The result has been a tightening of producer margins in 2023 and 2024.

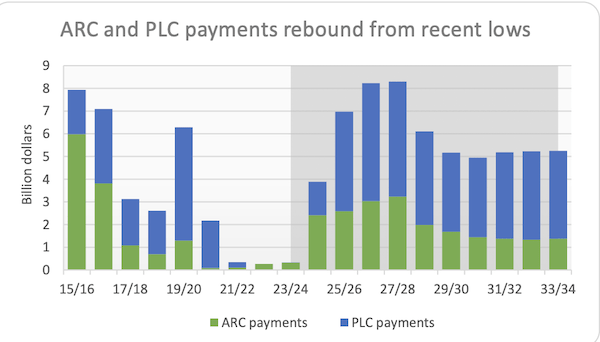

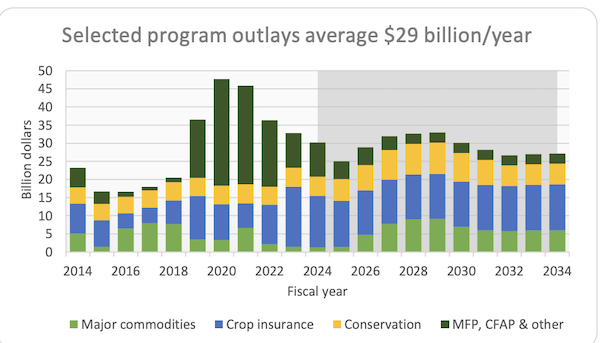

For commodity programs, FAPRI notes that while recent high prices have reduced federal spending, crop insurance net outlays still hit a record level in fiscal year (FY) 2023. Lower projected prices cause spending on the price loss coverage (PLC) and agriculture risk coverage (ARC) programs to rebound in future years.

- FAPRI expects total ARC and PLC payments to remain below $1 billion for the third straight year in 2023/24.

- From 2024/25 to 2027/28, however, the combination of higher payment triggers and lower projected market prices results in a sharp increase in ARC and PLC payments.

- Average payments decline after 2027/28, as effective reference prices and ARC benchmark revenues decline again.